|

The following is an email campaign from Brazil Potash . We do not endorse any specific company, product, or service mentioned in this email. Our mission-critical

information is sent each weekend and is separate, therefore unsubscribing from this email will also stop your Free Morgan Report subscription.

| |

| |

In The Sweet Spot For Potash

Profits Located nearby a prolific agricultural region, one potash developer expects to shorten product shipping times from 100+ to 2.5 days,

cutting costs roughly in half.

Its name is Brazil Potash (GRO.NYSE-A) and its Autazes project all alone could supply up to 20% of Brazil's annual potash demand…and make investors a bundle in the process.

Dear Investor,

A severe fertilizer supply crunch

has countries around the globe looking to domestic sources of key commodities like potash.

Consider this: Brazil imported ~98% of its potash in 2021 from an international market dominated by Canada, Russia and Belarus.

That dependence leaves Brazil's $167 billion agricultural sector completely vulnerable to price volatility, geopolitical risks, and supply disruptions.

And that's where

Brazil Potash

(GRO.NYSE-A) comes in.

The company has a project in the Amazonas Basin in northwest Brazil that expects to produce up to 2.4 million tons of potash annually.

That puts its vast potash resource within easy barging distance of one of the world's most prolific agriculture regions.

As you're about to see, that location gives Brazil Potash a huge competitive advantage over its larger competitors with projects in other parts of the world.

Brazil Potash's Autazes project has the

potential to generate an eye-popping ~$1 billion per year in earnings over its mine life of at least 23 years, and the company has received all of the construction licenses that it expects to be required to initiate the construction of the Autazes project.

That makes this the perfect time for investors to take a close look at Brazil Potash.

Amazonas Basin Location Provides Huge Competitive Edge

As one of the largest agricultural exporters in the world, Brazil plays a pivotal role in global food production, responsible for 1 in every 10 meals consumed worldwide.

Yet, despite being an agricultural powerhouse, Brazil faces a critical supply chain problem. Brazilian farmers consume over 20% of the world's

seaborne potash, yet they pay a steep premium due to long-haul shipping costs and supply chain inefficiencies.

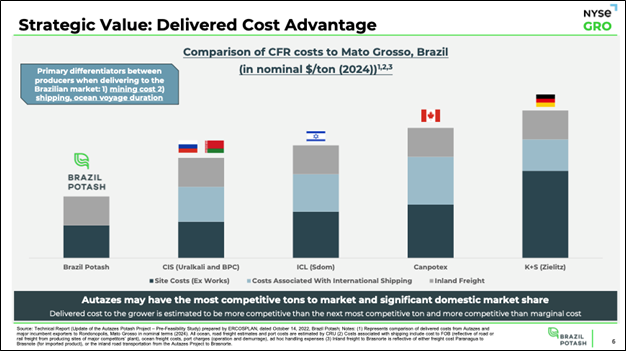

As the chart below indicates, much of the cost of potash is related to shipping it across long distances.

|

| | |

Alt Text: Chart comparing the total delivered costs of potash to Brazil's Mato Grasso region from Autazes and various international potash mines.

|

|

| | Brazil Potash (NYSE-A:GRO) is positioned to change that. Strategically located near one of the world's most productive farming regions, Autazes offers a clear competitive edge over legacy potash producers.

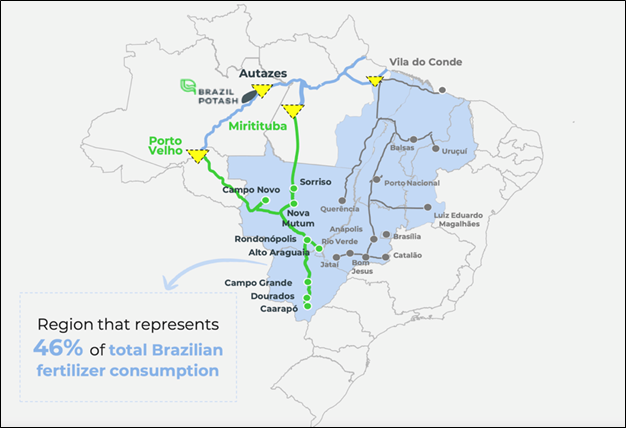

As this map makes

clear, Autazes is located within easy shipping distance of the main farming regions in Brazil, which accounts to 46% of Brazilian fertilizer consumption.

|

|

| |

Alt Tex: Map of Brazil with its key agricultural region highlighted in light blue

|

|

| Brazil Potash's Autazes project's location in the country's Amazonas Basin puts it within easy inland shipping distance of its main agricultural region.

The transit time for shipping potash from Autazes is estimated to be just 2.5 days as opposed to the 100+ day shipping timelines for potash from Canada or Russia.

That dramatic difference in shipping times translates into big savings... and a huge advantage for Brazil Potash by cutting costs roughly in

half.

The company believes that the resource at Autazes is large enough to meet roughly 20% of Brazil's demand for potash, with a projected production of up to 2.4 million tons of potash annually. And while the mine is initially expected to operate for 23 years, this estimate is based on exploration of only ~5% of the project's

basin.

With further exploration, management believes the resource could potentially support production for multiple generations.

Run By Industry Titans

In a strong signal of how lucrative the opportunity at Brazil Potash could be, the company drew the leadership of Mayo Schmidt. He is the former Chairman and CEO of Nutrien - the world's largest potash producer.

Schmidt has first-hand experience scaling billion-dollar operations, and he has a deep understanding of the potash market. Under his guidance, Nutrien's annual revenues shot up from $9 billion to $28 billion, a 318% gain.

He is the founder and former CEO of Viterra Inc.,

a company he built from a ~$40M regional cooperative to a global business with ~$800M in EBITDA over a 12-year period prior to being acquired by Glencore.[ii]

He's held senior positions in ConAgra Grain, General Mills, and Hydro One Limited - Canada's largest utility. And he served on Agrium's board of directors, overseeing a transformative merger with Potash

Corporation to form Nutrien that catapulted the company to global recognition.

The chance to take over a company and a project that could supply up to 20% of Brazil's potash demand was simply too good for him to pass up.

He's

joined by an advisory board that includes the former Attorney General of Brazil, the former Minister of Agriculture, and the former Senator of the largest farming region in Brazil and SALIC's (Saudi Agriculture and Livestock Investment Company) former head of Agriculture Supply Chain Investments.

Schmidt shepherded Brazil Potash through a $30 million IPO in November

2024. Such was Wall Street's enthusiasm for the company's story.

That interest has already begun to materialize. In November, Franco-Nevada, one of the world's largest royalty and streaming companies, secured an option to purchase a 4% royalty on gross revenue in exchange for the payment to Brazil Potash of cash consideration of $1,000,000-a move that underscores

institutional confidence in the long-term viability of the Autazes project.

The project's clear logistical advantage was not lost on Franco-Nevada. While established producers may have the size, expertise, and resources - when it comes to the economics of selling potash into Brazil, they are at a major transportation distance and resulting cost disadvantage. The

moment this new source of potash enters the supply chain, Brazil Potash could capture market share.

A Growing Pipeline Of Partners

After 14 years of exploration, ~$250 million invested, and mine construction set to begin, the project is at a pivotal moment. Key permits are in place, marking a major step toward full-scale development. A dedicated onsite processing plant will enable rapid refinement and distribution.

Brazil Potash is now securing strategic partnerships to pave the way for future planned production.

The Amaggi Group, a soybean producer with ~$10 billion in annual revenue, has already agreed to a 550,000 tons per year offtake agreement with the company.

Another firm, Swiss-based fertilizer trader Keytrade, has entered into a memorandum of understanding for potential offtake of up to one million tons per year of potash from the project.

And to further cement their logistical advantage, Brazil Potash has secured a 15-year shipping agreement with Hermasa, which

includes exclusive river barge transport rights. This ensures a consistent supply chain to Brazil's major farming regions.

More partners are in the works, and it looks like Brazil Potash is uniquely positioned to build an in-demand, Brazil-centric mine at Autazes.

Potash Companies Can Trade At Up To Nine Times EBITDA

With key permits for construction of Autazes obtained, offtake agreements rolling in and a 15-year river barge

agreement in place, Brazil Potash is set up to dramatically shorten the supply chain for the country's agricultural sector.

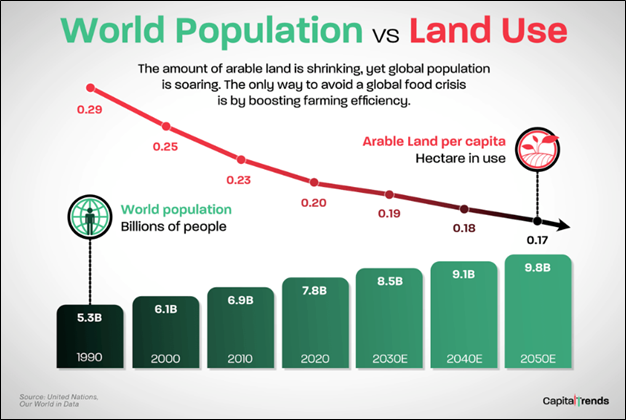

The importance of this project extends even beyond Brazil's borders. That's because, as the world's population grows toward 9.8 billion people in 2050, the world's arable land per capita will steadily drop. |

|

| |

Alt Text: Chart comparing increase in global population to the per

capita amount of global arable land.

|

|

| The world's population is growing while its per capita amount of arable land is shrinking, which

puts a premium on yield-increasing fertilizers like potash.

To feed that surge in population, the agricultural sector will have to do more with less land...and that means using fertilizers like potash to increase yield.

No wonder potash companies are predicted to trade at as much as nine times EBITDA in the course of the next market

cycle.

Autazes is projected to generate ~$1 billion annually in EBITDA over its at least 23 year mine life, and Brazil Potash is currently trading at just under $100 million. The upside potential with Brazil Potash is obvious.

The company is closing in on making a production decision on Autazes, making now a great time to do your research.

To Learn More about Brazil Potash Corp. |

|

| | Brazil Potash

FORWARD LOOKING STATEMENTS. This publication contains forward-looking statements, including statements regarding expected continual growth of the featured company and/or industry. The Publisher notes that statements contained herein that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect the companies' actual results of operations. Factors that could

cause actual results to differ include, but are not limited to, government regulations concerning potash production, the size and growth of the market for potash, the companies' ability to fund its capital requirements in the near term and long term, pricing pressures, etc.

Information contained herein has been obtained from sources believed to be reliable, but there is no guarantee as to completeness or accuracy. Because individual investment objectives vary, this Summary should not be

construed as advice to meet the particular needs of the reader. Any opinions expressed herein are statements of our judgment as of this date and are subject to change without notice. Any action taken as a result of reading this independent market research is solely the responsibility of the reader.

The Morgan Report is not and does not profess to be a professional investment advisor, and strongly encourages all readers to consult with their own personal financial advisors, attorneys, and

accountants before making any investment decision. The Morgan Report and/or independent consultants or members of their families may have a position in the securities mentioned. Mr. Morgan does consult on a paid basis both with private investors and various companies. Investing and speculation are inherently risky and should not be undertaken without professional advice. By your act of reading this independent market research letter, you fully and explicitly agree that The Morgan Report will not

be held liable or responsible for any decisions you make regarding any information discussed herein. |

|

|

Copyright © 2025 The Morgan Report, All rights

reserved |

|

|

|

|