|

This is a paid advertisement for Lodestar Metals. We do not endorse any specific company, product, or service mentioned in this email. Our mission-critical information is sent each weekend and is separate, therefore unsubscribing from this email will also stop

your Free Morgan Report subscription.

|

| | |

Lodestar Metals: Early-Stage Upside in Nevada with a Defined Roadmap |

|

|

In today’s precious metals environment—where rising gold and silver prices are reigniting exploration interest—the junior mining sector continues to offer compelling upside opportunities. While some investors have been taking profits in recent weeks, the search for undervalued names is intensifying, with a select few still trading at attractive valuations and offering

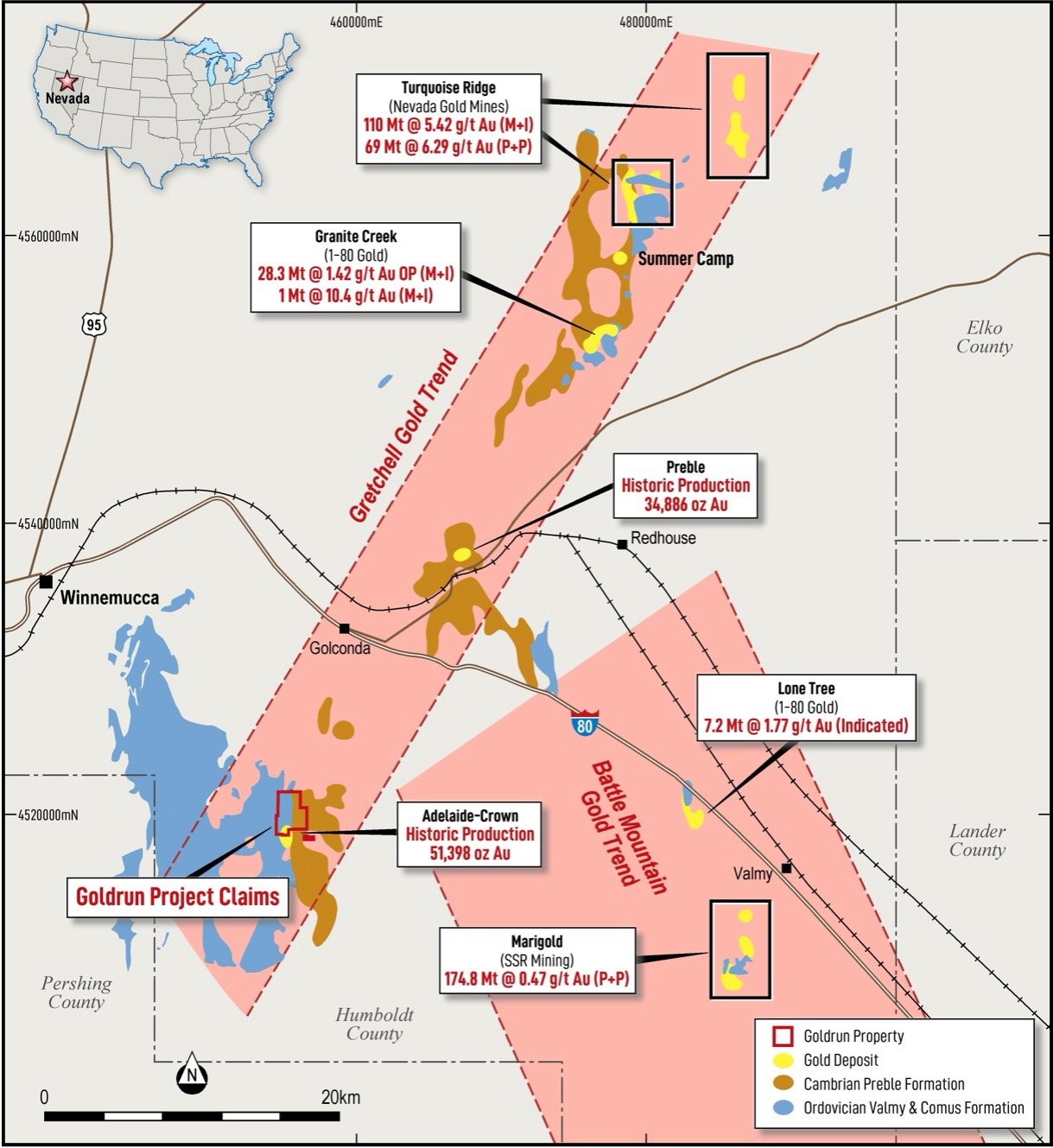

stronger upside potential than their peers. One such name deserving a closer look is Lodestar Metals Corp. (TSX-V: LSTR | OTC: SVTNF), which is advancing a project in Nevada with a modest enterprise value and a defined exploration strategy. Project Location & JurisdictionLodestar’s key asset is the Goldrun Property, located in Humboldt County, Nevada, USA. According to the Company, it comprises about 75 unpatented claims (~516 hectares) arranged in two non-contiguous blocks. Nevada remains a top-tier jurisdiction for gold and silver exploration and mining. The Company notes that approximately 80% of U.S. gold

production occurs in Nevada; the region produced some 4.2 million ounces of gold in 2023 and accounted for nearly 5.3% of global production in that year. Additionally - the company is evaluating additional gold and silver opportunities in the district, further increasing potential value. The message is clear: the location is favourable from a regulatory, infrastructure and geological framework standpoint. Geology, Legacy Work & Upside PotentialLodestar emphasises that Goldrun lies within the “Gretchell Gold Trend,” and is in a similar structurally complex setting to the well-known Turquoise Ridge deposit (Barrick Gold) in the Battle Mountain Trend.

Historical work on the project includes: - A non-compliant historical estimate (by FMC Gold Co. in 1991) of 50,000 to 100,000 ounces of gold at 0.037 to 0.067 opt (~2.1 to 2.1 g/t) in discontinuous mineralised zones. Note: Lodestar flags this as “historical” and not NI 43-101 compliant.

- 131 drill holes totalling 17,823 m (˜58,500 ft) of historic drilling, many holes shallow (<50–100 m) and vertical.

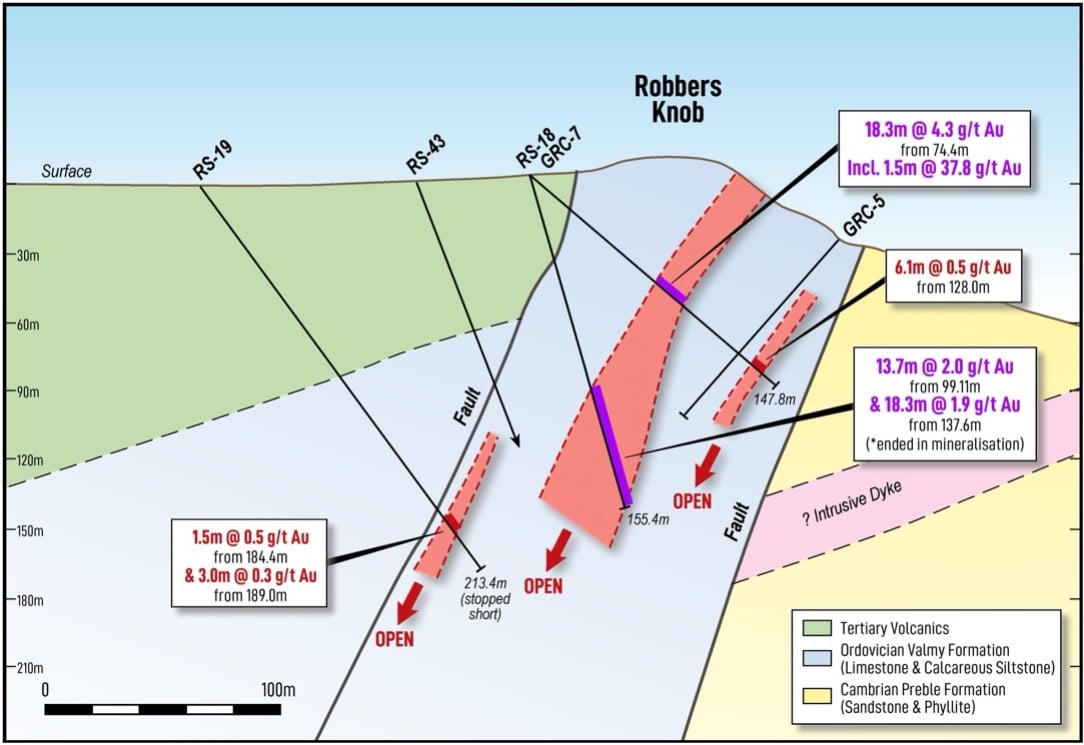

- Significant intersections reported historically such as 18.3 m at 4.3 g/t Au including 1.5 m at 37.8 g/t Au in the Robbers Knob prospect.

- Surface rock sampling by

Lodestar (15 samples) returning widespread gold as well as high-grade silver — up to 3,307 g/t Ag and 546 g/t Ag, with gold up to 2.7 g/t Au on the “Independence Trend”.

The implication: while no current compliant resource has been declared, the footprint appears under-explored with multiple compelling targets that are “drill ready”. Strategy & Expected Exploration ProgramLodestar outlines a systematic, phased exploration strategy:- Phase 1 – Target Definition (Completed):

Apply modern-day exploration techniques, including soil geochemistry and high-resolution UAV magnetic surveys, to refine and rank targets. This work has identified three extensive, kilometre-scale gold–silver soil

anomalies across the Gold Run Property, with peak values of up to 298 ppb Au and 33 g/t Ag. Distinct metal assemblages suggest the presence of both Carlin-style and epithermal-style mineralization systems, supporting multiple compelling exploration targets. Historical DDIP data along the Gomes and Independence Trends has further advanced several areas to drill-ready

status.

- Phase 2 – Initial Drilling & Expanded Geophysics (Q1/Q2 2026):

Execute a maiden drilling program on the highest-priority targets (including Robbers Knob, Gomes, and Grindstone Flats), alongside

a project-wide DDIP geophysical survey. With Phase 1 complete, Lodestar is finalizing plans for both a maiden diamond drill program and expanded DDIP coverage, with programs expected to commence in Q1/Q2 2026. This phase represents a key value inflection point, as the Company moves from target definition to direct testing of priority zones.

- Phase 3 – Advancement & Growth:

Follow-up drilling, definition drilling, resource estimation, and strategic expansion (including deeper drilling and broader project growth) in subsequent phases, contingent on results.

Given the Company’s modest market capitalization (approximately C$7.64 million at the time of presentation) and 43.67 million

shares outstanding, Lodestar offers what can reasonably be described as high-leverage exposure to exploration success, particularly as Gold Run remains largely untested by drilling despite its strong technical foundation and location within a proven Nevada mining district. Why the Potential Upside Could Be Material- Jurisdictional Advantage: Nevada’s status as a “tier-1” gold jurisdiction lowers permitting and infrastructure risks that plague more remote jurisdictions.

-

Footprint & Historical Data: The project has a large alteration footprint (20 km² of surface alteration in one prospect; 600m×250m jasperoid massif at Robbers Knob) and multiple indications of gold-silver mineralisation (see image below), including high-grade rock samples,

which is a favourable starting point.

|

|

| | | |

|

- Low Entry Cost: With limited modern exploration carried out and a small current valuation, the project could benefit significantly from positive drill results.

- Clear Roadmap: The step-wise strategy improves transparency and milestones are definable: soil/geo

surveys -- drill targets -- maiden drilling -- resource definition.

Key Risks & Considerations

- No Current NI 43-101 Resource: The historical resource estimate is non-compliant and cannot be relied upon as definitive.

- Exploration Risk: As with any early-stage exploration company, there is inherent risk in discovery — drilling may not deliver economic

grades, or the footprint may be smaller than anticipated.

- Commodity Price Sensitivity & Execution Risk: The economics of any future deposit will depend on gold and silver prices, as well as mining, processing and permitting challenges.

Final Thoughts

For investors focused on the junior mining sector

and comfortable with exploration-stage risk, Lodestar offers a well-situated asset in a proven mining jurisdiction, with multiple strike-length targets, historical drilling and surface indications of both gold and silver. Importantly, the Company currently trades at a valuation that appears attractive relative to comparable early-stage explorers with similar

jurisdictional quality and target scale, suggesting the market has yet to fully price in the project’s geological potential.

The key is execution — achieving successful first-pass drilling or even high-grade intercepts would meaningfully derisk the story and could unlock upside in a modest valuation vehicle.

While this is not a “safe” or “guaranteed” story, the risk/reward profile suggests a compelling speculative opportunity: if the

Company delivers according to plan on its defined road-map-as they have demonstrated so far-then the potential upside could be significant especially when viewed against the current valuation and peer benchmarks in the junior exploration space.

For new investors - keep an eye on drill results and any strategic partner announcements. If any

of those items come positive, then the market may begin to ascribe a higher valuation to the story, which should help the company on their drill programs going forward.

Website:

https://lodestarmetals.ca

Investor RelationsEmail: investors@lodestarmetals.ca |

|

| | Information contained herein has been obtained from sources believed to be reliable, but there

is no guarantee as to completeness or accuracy. Because individual investment objectives vary, this Summary should not be construed as advice to meet the particular needs of the reader. Any opinions expressed herein are statements of our judgment as of this date and are subject to change without notice. Any action taken as a result of reading this independent market research is solely the responsibility of the reader.

The Morgan Report is not and does not profess to be a professional

investment advisor, and strongly encourages all readers to consult with their own personal financial advisors, attorneys, and accountants before making any investment decision. The Morgan Report and/or independent consultants or members of their families may have a position in the securities mentioned. Mr. Morgan does consult on a paid basis both with private investors and various companies. Investing and speculation are inherently risky and should not be undertaken without professional advice.

By your act of reading this independent market research letter, you fully and explicitly agree that The Morgan Report will not be held liable or responsible for any decisions you make regarding any information discussed herein.

|

|

| Brought to you by: The Morgan

Report |

|

|

|

|