This matters because copper is not just a construction metal anymore.

It is the backbone metal for electricity, and electricity is the bottleneck behind AI, data centres, RAM heavy compute, and the grid buildout that has to follow.

The result is simple.

Even if copper cools off for a stretch, the longer term setup is still

tightening.

At the same time,

Abitibi Metals Corp. (CSE:AMQ) (OTCQB:AMQFF) is doing the one thing a junior must do to stay relevant in a real metals

tape.

Deliver drill results that change the conversation.

Not theoretical.

Not legacy.

Not a story that needs ten slides to explain.

A hole that forces the market to pay attention.That is what happened at B26.

In hole 1274 17 269W5, Abitibi Metals reported 13.48% copper and 5.15 g/t gold over 6.3 metres, which

equates to 17.91% copper equivalent.

Inside a broader 19.5 metre zone grading 6.93% copper equivalent.

That is not a "nice intercept."

That is the type of interval that makes serious technical teams stop scrolling and start modeling.And it was not a one off.

Another newly reported hole returned 4.46% copper equivalent over 21.1

metres, inside a broader 69.0 metre envelope grading 1.8% copper equivalent, plus 3.93% copper equivalent over 11.0 metres in a separate interval.

Put those together and the asset starts to read differently.

B26 is showing thickness.

It is showing repeatability.

And it is showing the kind of higher grade shoots that can materially change how the next resource update is framed.

Now layer in the macro.

Here is why copper can still move much higher over the

longer term, even if it chops around short term.

- Data centres and AI are becoming a real copper demand engine: BHP estimates copper used in data centres could grow six fold by 2050, from around 0.5 million tonnes per

year today to about 3 million tonnes per year by 2050. (BHP)

- Power grids are the bottleneck, and the investment is real: Reuters reports grid expansion and modernization is accelerating, with record investment levels, and demand rising from data centres

and electrification. (Reuters)

- The supply side is structurally slow: S&P Global reported the IEA warning that copper could face a supply deficit that reaches 30% by 2035, driven by constraints like declining ore grades, capital intensity, and long

timelines. (S&P Global)

- The capital required is enormous: BloombergNEF continues to frame the transition metals buildout as a multi trillion dollar investment requirement through mid century, with mining investment needing to rise meaningfully to keep

up. (BloombergNEF)

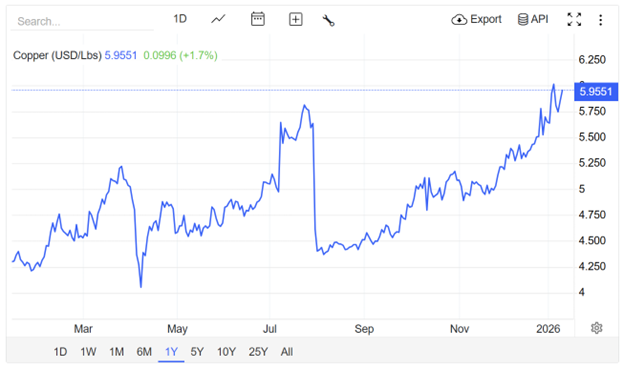

This is why the chart matters.

The chart is not just price action.

It is the market slowly waking up to a supply problem that cannot be solved quickly.

Now look at:

Abitibi Metals Corp. (CSE:AMQ) (OTCQB:AMQFF)