Dear Reader,

Below is an alert on a company by the name of Fireweed Zinc (TSX-V: FWZ)

from my colleague Eric Coffin, editor of HRA Advisories. Eric is a very well

respected newsletter writer, focused on the junior mining space.

Fireweed just released an impressive resource calculation update and Eric

(as he does) breaks it down clearly for his subscribers below. You'll want

to read this overview too, as this is a company that still has huge upside

potential, as you'll read below.

Sincerely, David Morgan

GROWING LIKE A WEED

JANUARY 10, 2018

Fireweed Zinc (FWZ-V; Halted at $1.24) released an updated resource

calculation for the Tom and Jason zones on its MacMillan Pass project this

morning. I think its fair to say the resource exceeded all expectations. I

had come around to thinking we would see a pretty large bump up from the

2007 version, but the reality is even more impressive than my internal

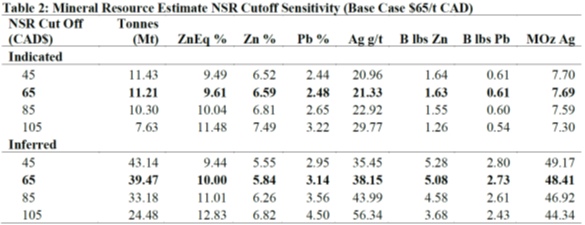

guesses. The new resource includes 11.21 million Indicated tonnes grading

6.59% zinc, 2.48% lead and 21.3 g/t silver and 39.47 million Inferred tonnes

grading 5.84% zinc, 3.14% lead and 38.15 g/t silver using the base case NSR

cut off of $65CAD/tonne.

The table below shows the resource estimate using several different NSR cut

offs. The new resource incorporates 25 drill holes completed by either

Fireweed or HudBay since the date of the previous estimate. As I noted in

the last couple of FWZ updates, several 2017 drill holes returned higher

grades and, in some cases, far larger widths than anticipated from modelling

of historic results. This would have contributed to the increase in tonnes.

The current estimate used 40 metre maximum drill hole spacing for Indicated

resources and 100 metres for Inferred resources. That is still conservative

for a Sedex deposit as they generally have fairly predicable geometry. The

news release notes that the current estimate includes more accurate specific

gravity than the 2007 version. The s.g. number used was not specified but

the old version was low for this kind of material. Using a new and more

accurate one would have added tonnage as well.

The NSR was calculated using three-year trailing and two year forward

estimates for metals prices and incorporates metallurgical recoveries from

historic met work that indicated recoveries of 79% for zinc, 82% for lead

and 85% for silver. Using spot prices and exchange rates the NSR would be

more like $100/t CAD which seems reasonable. The estimate includes

calculations done using higher cut offs. At an $85/t cut off the resource is

still above 43 million tonnes with a zinc equivalent grade of just above

10%.

|

"This is a very impressive resource upgrade. Tom-Jason is now one of the

largest undeveloped zinc lead resources in the world that is not controlled

by a base metal major." |

And it's not done growing. There are a couple of outlier historic holes that

could not be included in the resource (including one that reported 14% zinc

over good widths 200 metres from the resource envelope) and the currently

modelled zones are open in several directions. There are several targets on

this large project that have not even been drill tested yet. The resource

really doesn't need to be any bigger given the probable mining rates, but

traders do like to see new zones and new high-grade intercepts. As it

stands, Tom-Jason has the potential to be quite a long lived mine, something

that will appeal to potential acquirers.

I expect Fireweed will complete a financing before the start of this year's

field season and hit the ground running with a much larger drill program. In

the meantime, we will get the first pass PEA study for the project that will

give us the first read on the potential economics for Tom-Jason. Given the

size and grade of the new resource I don't expect that study to be a

disappointment. Fireweed has a strong technical management team with plenty

of Yukon experience. I have little doubt that there have been plenty "back

of the napkin" calculations done internally as I don't see these guys

pushing this hard on the project unless they were already comfortable the

numbers would work.

In terms of valuation, there are not a lot of comparable companies that have

resource in the new improved Tom-Jason size range. The only one that comes

to mind is Tinka (TK-V) that recently released an updated resource for its

Ayawilca project in Peru of 42.7 million tonnes Inferred with a zinc

equivalent grade of 7.3% using a similar NSR cut off. Tom-Jason has 20% more

tonnes (some Indicated) at a 35% higher zinc equivalent grade. I'm not

trying to take anything away from Ayawilca which is an excellent deposit but

I don't think its logistics are superior enough to account for the valuation

differences between FWZ and TK. At the share price Fireweed was halted at

its market value is about $20 million, while TK's valuation is almost eight

times higher at $170 million. Clearly, based on comparables alone, Fireweed

has a huge amount of potential upside and is a strong buy at current prices.

I encourage you to sign up to receive future news and updates from Fireweed

Zinc: www.fireweedzinc.com

Regards for now:

Eric Coffin

|

Do you want to learn about stories like these ahead of the crowd? I

initially told subscribers about Fireweed Zinc in April 2017, pre-IPO at 50

cents. It is now trading in the $1.30 range (as of Jan. 10, 2018).

Getting gains like this IS possible when you are a subscriber to HRA

Advisories.

Click here to subscribe to HRA at no risk - you'll receive a full refund

within 30 days if you decide this service isn't for you. But with a track

record like mine…183% gains on 119 closed positions, with 31 companies being

TAKEN OVER, can you afford not to give it a try?

www.hraadvisory.com |

HRA - Special Delivery is an independent publication produced and

distributed by Stockwork Consulting Ltd, which is committed to providing

timely and factual analysis of junior mining and other venture capital

companies. Companies are chosen on the basis of a speculative potential for

significant upside gains resulting from asset-base expansion, new

discoveries and potential for future M&A activity or movement through

development to production. These are generally high-risk securities, and

opinions contained herein are time and market sensitive. No statement or

expression of opinion, or any other matter herein, directly or indirectly,

is an offer, solicitation or recommendation to buy or sell any securities

mentioned. While we believe all sources of information to be factual and

reliable we in no way represent or guarantee the accuracy thereof, nor of

the statements made herein. We do not receive or request compensation in any

form in order to feature companies in this publication. We may, or may not,

own securities and/or warrants to acquire securities of the companies

mentioned herein. If we're buying a financing in a company HRA follows we

say so and we pay for it with our own cash, the same as you. HRA

publications are as much as anything about what I am doing with my own

resource investing so if I talk about a company its safe to assume I own it

or plan to shortly. This document is protected by the copyright laws of

Canada and the U.S. and may not be reproduced in any form for other than

personal use without the prior written consent of the publisher. This

document may be quoted, in context, provided proper credit is given.

Published by Stockwork Consulting Ltd. Box 85909, Phoenix AZ, 85071.

customerservice@hraadvisory.com

| www.hraadvisory.com

Subscriptions/Customer Service 1-877-528-3958