|

"Buy low, sell high"

distills business and investing to its essence.

With gold poised for a bull market, the first and

biggest winners are those with established National

Instrument 43-101 gold resources with leverage to higher

prices.

AND GoldMining Inc. is the best stock to multiply your

returns on the yellow metal.

We know that much higher gold prices are

inevitable... And it's very likely that the next move

will usher in a bull market similar to the one we saw

from 2004 until 2011 when gold prices exceeded

US$1,800oz. When that happens, Companies that can

accumulate assets on the cheap during down markets stand

the best chance of outperforming their peers when bull

markets re-emerge.

What makes GoldMining a

compelling play on gold?

GoldMining Inc. (GOLD.TSX;

GLDLF.OTCQX) amassed 9.5 million ounces of gold

resources in the measured and indicated categories along

with an additional 11.7 million ounces in the inferred

category with numerous advanced exploration projects

across the Americas in 5 safe jurisdictions.

The Company has executed to perfection and it did so

by leveraging the down market for gold to buy assets at

fire sale prices - in some cases at less than US$1/oz.

That's the story.

How the right gold equities can offer investors that

leverage on the yellow metal.

When gold prices rose in 2016 (about 25 percent from

$1,050 to $1,370), companies with established assets did

much better. But since 2011, the yellow metal has

largely traded down to sideways, negatively impacting

numerous junior exploration companies. The downturn

presented opportunities for

GoldMining Inc. to

scoop up companies and projects extremely inexpensively

all around the Americas in places like Alaska, Brazil,

Colombia, Peru and Canada.

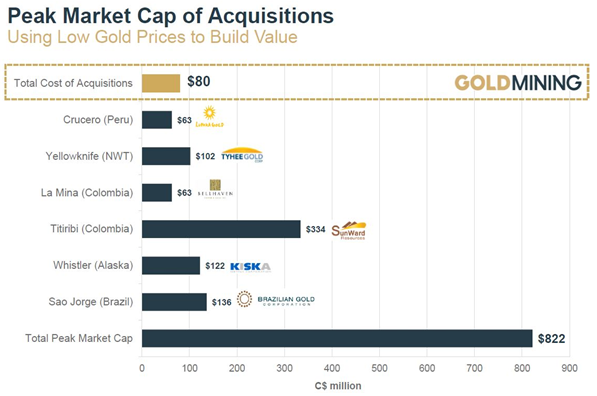

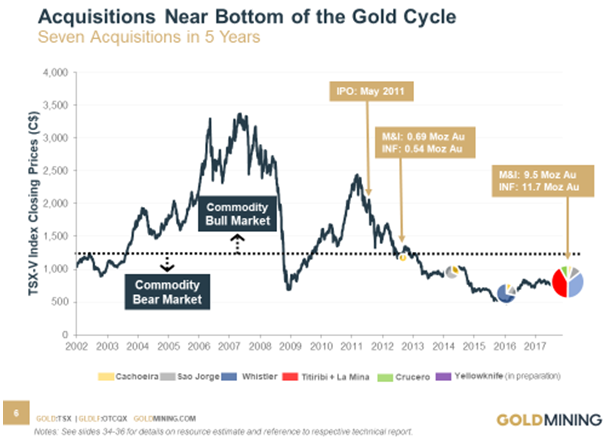

The following chart - showing the peak market caps of

the companies that

GoldMining has brought

into its portfolio - tells a compelling story.

Value and Optionality on a per share basis

If you look at the combined peak market cap of all the

companies that

GOLD acquired from

2012-17, you will observe that the Company paid C$80

million to acquire projects that were valued at C$822

million at their peak. Note that these transactions were

nearly all stock deals, consisting of shares with no or

very minor cash payments. The company's current market

cap hovers around C$120 million.

GOLD definitely made acquisitions well

below all-time peak market caps, historic values, and

replacement value.

A quick calculation shows

that its all-in global gold equivalent resources totals

12.4 Moz in the measured and indicated categories and an

additional 14.2 Moz of inferred (when factoring in 2

billion pounds of copper) are currently valued at less

than US$4 per ounce of gold in the ground! And that

is a compelling valuation compared to its mid-tier

junior exploration peers.

You read that right. If the next bull market brings the

projects in GoldMining's portfolio back to their peak

value, it would deliver nearly a seven-fold increase in

the company's valuation versus the current stock price

of ~C$0.90.

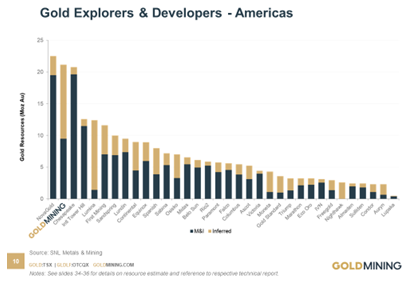

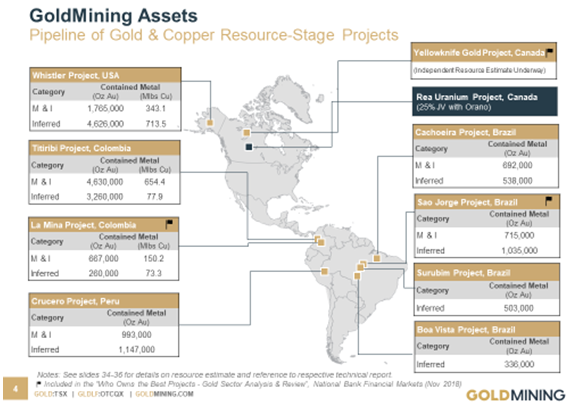

Large Diversified Portfolio of High-value Projects in

Politically-Stable Countries

GoldMining boasts 9.5

million ounces of gold in the measured and indicated

categories along with 11.7 million ounces in the

inferred category with 8 projects spread across the

Americas in safe mining jurisdictions: Alaska, Canada,

Brazil, Colombia and Peru.

That's key, because the market

often applies a political discount to projects and

companies operating in countries without strong

protections for foreign investment.

Plus,

GoldMining has some

optionality on uranium, thanks to a 75% interest it

holds in the Rea property in the Athabasca Basin. (Note:

uranium prices just hit a 52 week high on improving

fundamentals - this asset is becoming more valuable by

the day!)

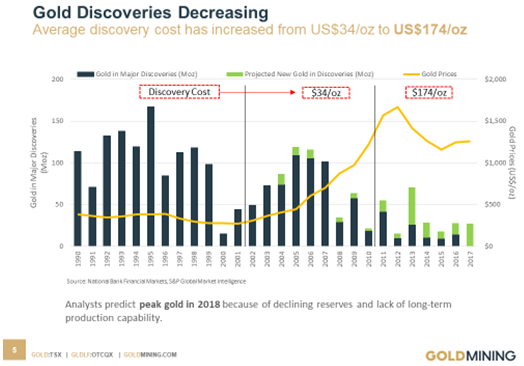

Best Optionality for High-leverage Gold Plays.

With exploration costs now averaging $174 per ounce

of gold discovered, GOLD has chosen a different tact.

In the past 6 years, the gold sector has

been beaten up leading to underinvestment by the majors

on exploration. Major producers are faced with declining

reserves and lack of long-term production capability,

which had led to increased mergers and acquistions in

the sector in the past 3 months (i.e. Barrick and

Randgold, Newmont and Goldcorp). Companies with a single

asset are faced with high operating costs and

geopolitical and operations risk to preserve thier

project and cash.

GoldMining has been

able to identify exceptional opportunities, cut good

deals and do it consistently, and do it patiently at the

bottom of the cycle.

Since the company's IPO in 2011,

GoldMining has taken

advantage of the prolonged bear market to acquire

resources in the ground for less than $10 an ounce, way

below the unit discovery cost today. Keeping G&A cost

per ounce at bare minimum preserves the longevity of

that option value on a massive gold resource on a per

share basis. For an investor, it's like holding this

multi-year optionality in your hand for the long term.

Distressed companies or resource project assets acquired

by

GoldMining had already

spent hundreds of millions in completing a large amount

of work on these sizable gold-copper advanced

exploration-stage projects. This includes completed

drill programs, NI 43-101 technical reports, and even

pre-economic assesments (PEAs) that are attractive to

mid-size and large gold companies who are searching to

add ounces to their portfolios now.

Assuming these projects are ultimately sold-off for

significant cash or spun-out individually into other

companies when the inevitable bull market for

commodities comes around, future transactions will

result in significant capital gains to GOLD

shareholders.

Is NOW the time to get positioned in GoldMining Inc?

GoldMining was publicly trading during the 2016 precious

metals rally when

GOLD was the #1 top

performing gold stock on the Toronto Venture Exchange.

During this time frame,

GOLD stock zoomed from

C$0.38 in January 2016 to C$3.35 in September for a

return of nearly 9x!

The record shows the

GoldMining had an EV/oz

of US$20/oz. in June of 2016 versus todays EV/oz of

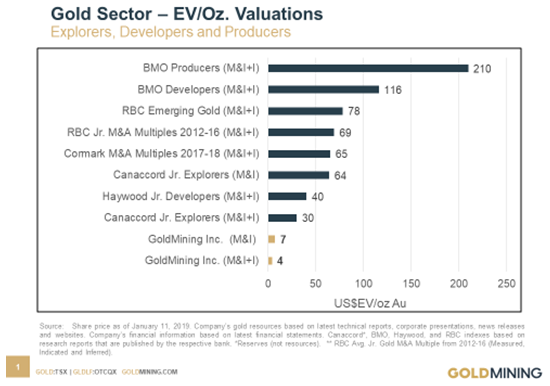

US$4/oz even though GoldMining has increased its global

resource by 108% during this time.

That's 5 times today's level of US$4/oz. - and an

indication that a resurgence of gold to just its 2016

prices could send GoldMining's share price soaring

towards new all-time highs!

GOLD stock purchased in mid-December 2016 at C$1.50 and

sold five trading days later at C$2.25 returned 50%.

GOLD stock purchased in early December 2017 at C$1.25

and sold in mid-January 2018 for C$1.50 returned 20%.

GoldMining Inc is in a financially strong position

with over C$9 million in cash and no debt.

With eight projects in five different countries across

the Americas today, GoldMining controls one of the

world's largest diversified gold resource portfolios of

any publicly traded junior gold company.

The correction in precious metals prices offers

interesting options if you continue to believe in the

gold bull market.

Gold was at the key crossroads in late 2018, and

finally moved above US$1,300 in January with the U.S.

Federal Reserve finally pausing on further interest rate

hikes. And if gold renews its assault on the US$2,000

mark, the sky is literally the limit for this

well-positioned gold company.

Those who invest in

GoldMining today -

before gold turns the corner - could be very glad they

did.

CLICK HERE

Learn More about GoldMining Inc. |